Spark Protocol Revenue Analysis

Spark Protocol Revenue Analysis

💰 Spark's Revenue Secret Revealed

Spark Protocol maintains consistent revenue performance with $174M projected annualized revenue as of June 2025. The protocol shows stability in its financial metrics, continuing the trend observed since late 2024.

Key points:

- Spark remains the dominant revenue generator, contributing 48% of total protocol revenue

- Revenue projections have held steady at $174M annually

- Protocol demonstrates sustained growth in the DAI ecosystem

SparkLend continues to serve as the primary DAI-focused money market protocol, leveraging direct liquidity from Maker.

Steady revenue growth for the protocol. $174m current projected annualized revenue⚡️

Annualized revenue has gone from $63m to $174m in just two months, almost a 3x. @sparkdotfi is the world's largest Onchain Capital Allocator and it's really just getting started. data.spark.fi/spark-liquidit…

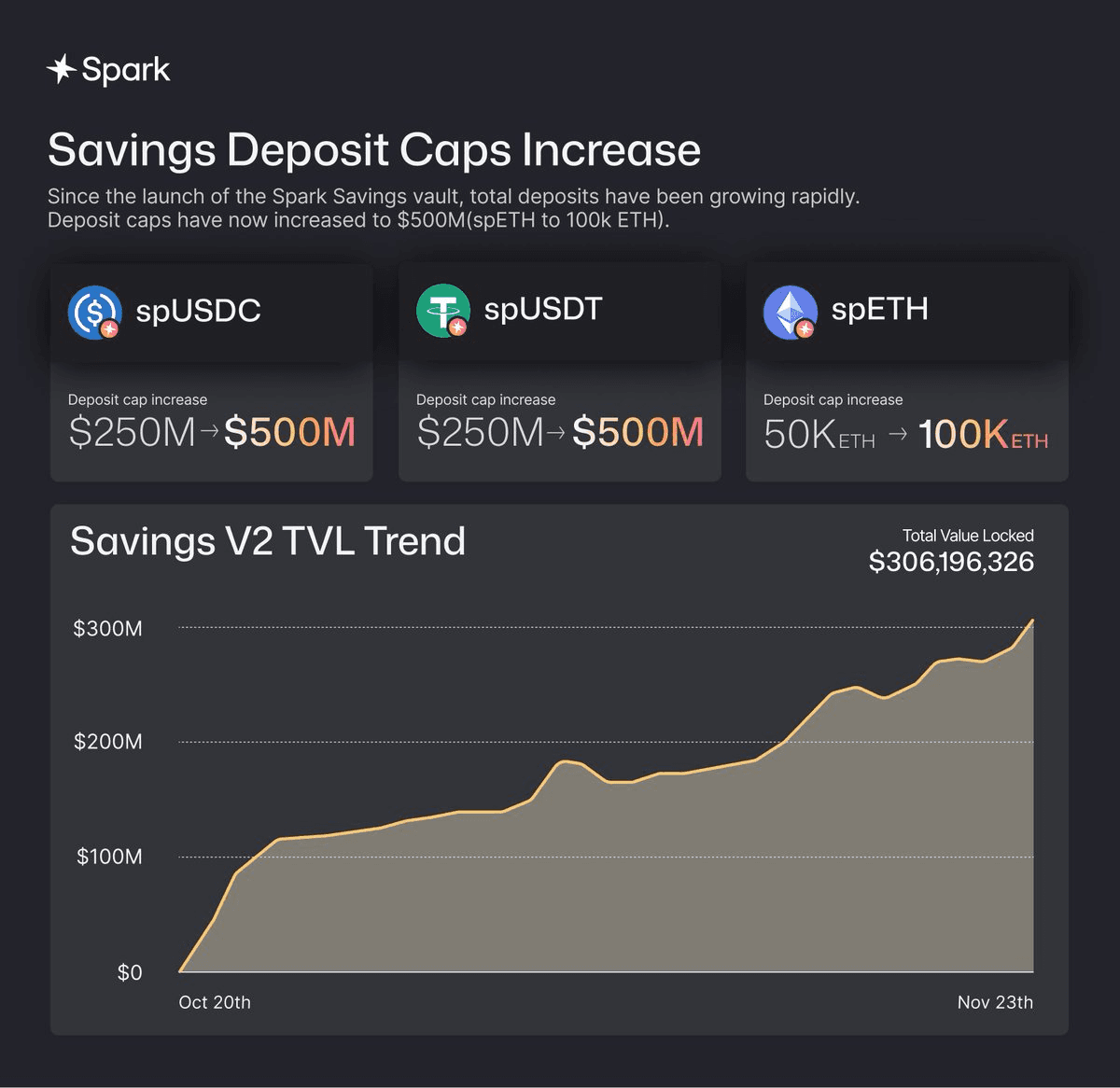

sUSDS Becomes Fastest Growing Asset in Spark Savings as TVL Hits $4.1B

**sUSDS has emerged as the fastest growing asset** within Spark Savings, driving significant growth across the platform. **Key Metrics:** - Total Value Locked (TVL) has **surpassed $4.1 billion** - Platform is hitting **new all-time highs daily** - Represents massive growth from previous milestones **Recent Growth Context:** - Savings V2 TVL previously reached $300M in November - Caps were raised to accommodate demand: USDT 500M, USDC 500M, ETH 100K - Spark now leads across all chains with +$3B in TVL **Platform Features:** - Institutional-grade, non-custodial access - Real-time compounding growth - No platform fees or slippage - Deposit stablecoins or ETH, withdraw anytime in same asset The rapid adoption of sUSDS demonstrates growing institutional and retail demand for yield-generating stablecoin products in the DeFi space.

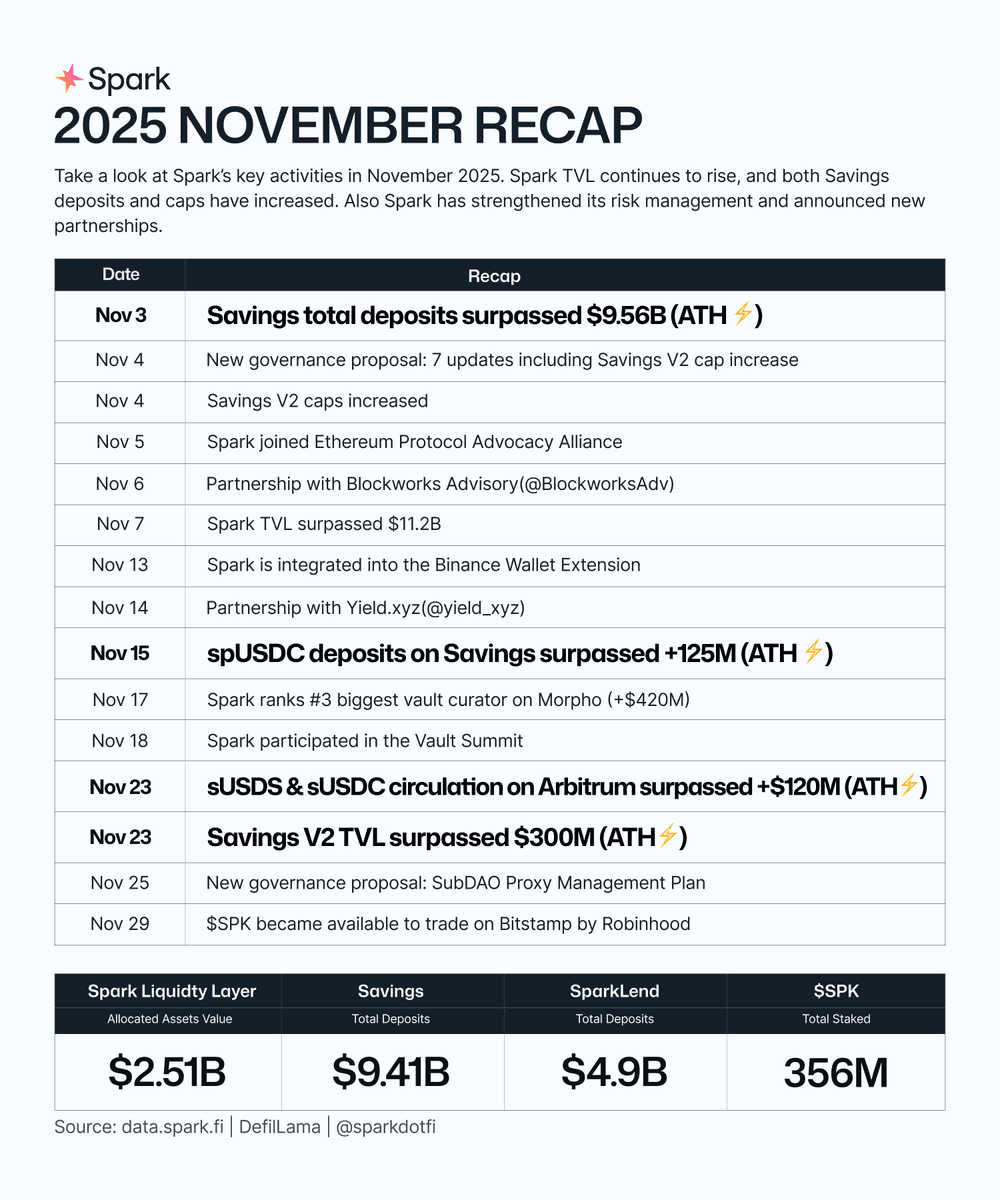

Spark Hits Multiple All-Time Highs in November

**Spark achieved multiple all-time highs** during November while delivering significant platform updates. The DAI-centric money market protocol continues its growth trajectory, building on previous monthly successes. Key developments included: - Multiple ATH milestones reached - Important platform updates delivered - Continued integration with top DeFi protocols Spark combines **premium liquidity from Maker** with vertical integration across leading DeFi platforms, strengthening the DAI ecosystem.

🔥 Two weeks left

**Spark Season 2 ending soon** - only two weeks remaining to accumulate points. Current stats: - **425+ billion points** distributed - **15,764 active wallets** participating This is your **final opportunity** to stack points before Season 2 concludes. [Start earning points now](https://app.spark.fi/points)

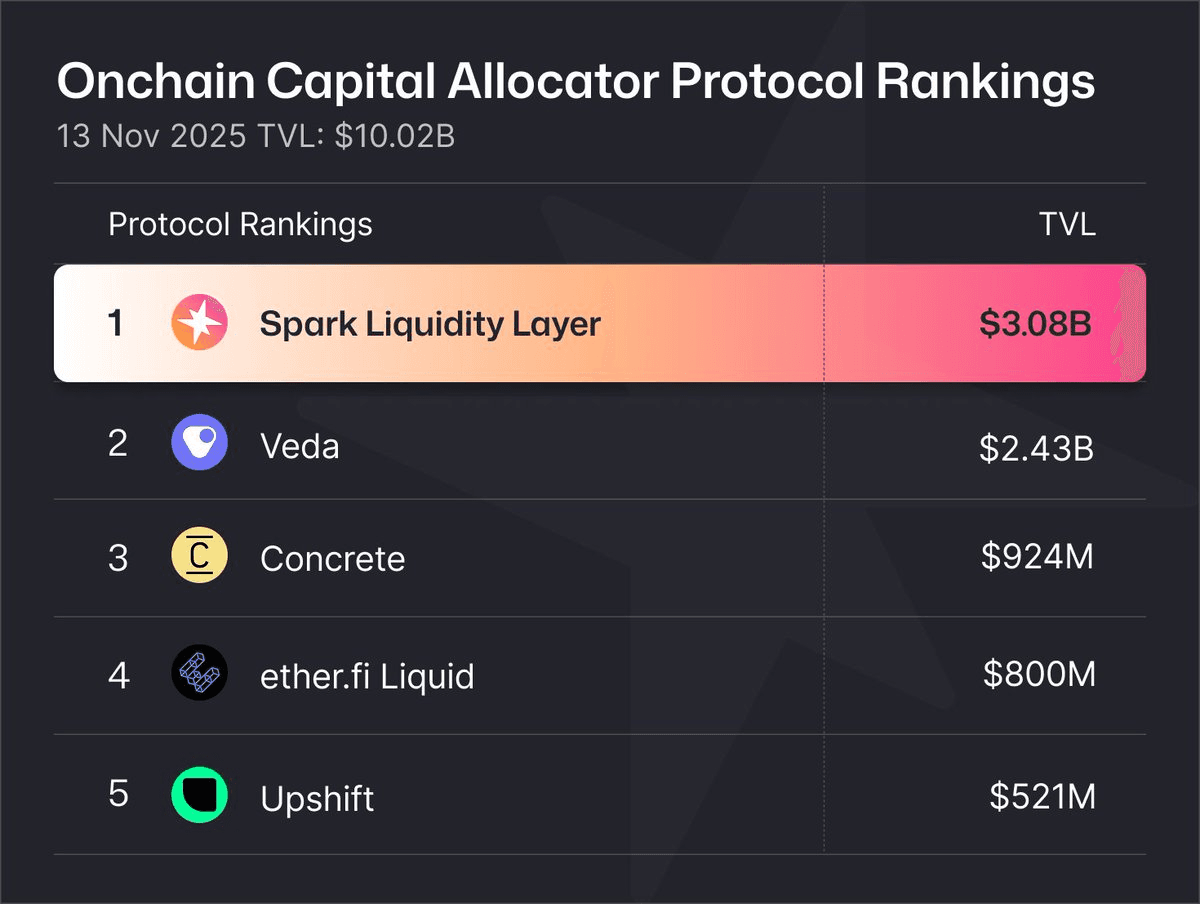

Spark Dominates $10B Onchain Capital Allocator Market with $3B TVL

The onchain capital allocator market has experienced explosive growth, expanding from $111M to **$10B in total value locked (TVL)** over the past 18 months. **Spark leads the market** across all chains with over $3B in TVL, demonstrating what institutional-grade DeFi protocols can achieve. This represents a **90x growth** in the overall market, highlighting the increasing adoption of onchain capital allocation solutions by institutional and retail users alike. The rapid expansion showcases the maturation of DeFi infrastructure and growing confidence in onchain financial products.

Last Call for Pendle Points Season 1

Final week to participate in Pendle Points Season 1, ending August 12, 2025. - Earn points by simply holding YT/PT-USDS positions on Pendle - No additional steps required - Access through [Spark.fi](https://app.spark.fi/points) or [Pendle Finance](https://app.pendle.finance/trade/pools/0xdace1121e10500e9e29d071f01593fd76b000f08) *Note: This crypto-asset marketing communication has not been reviewed by EU authorities. For official documentation, visit [spark.fi/mica](http://spark.fi/mica)*