Y2K Finance integrates Pyth Price Feeds on Arbitrum

Y2K Finance integrates Pyth Price Feeds on Arbitrum

Y2K Finance, a catastrophe bonds provider for DeFi, has integrated Pyth Price Feeds to resolve new markets and gain access to a range of new assets on Arbitrum. Users can buy insurance on depeg events and deposit assets in Y2K's Premium and Collateral vaults. Y2K currently supports 13 different assets and has seen over $150M in deposit assets.

IYKYK 🔮 @y2kfinance is a suite of structured products designed for exotic peg derivatives. #PoweredByPyth on @arbitrum, Y2K now has access to more assets. ℹ️ About Y2K Finance Launched a year ago, Y2K quickly became the most successful catastrophe bonds (CAT) provider for

Pyth Network Adds Intel Stock to Index Offerings

Pyth Network has expanded its index offerings to include **$INTC** (Intel Corporation stock data). The oracle network continues to build out its traditional finance data feeds, having recently added BRENT crude oil indices. Users can now access Intel stock data alongside other Pyth Indices. - Access available at [pyth.network/indices](https://pyth.network/indices?utm_source=organic_social&utm_medium=x_post&utm_campaign=2607_post&utm_term=pythindices) - Follows pattern of adding traditional market data to blockchain oracles - Part of ongoing expansion of real-world asset data feeds Pyth operates as a first-party oracle network, providing price feeds and market data to blockchain applications.

Hyperliquid Processes $400B in Trading Volume Using Pyth Oracle Data

Hyperliquid has processed **$400 billion in trading volume** over nine months, with **99.8% of prices sourced from Pyth Network**. The platform operates as a **24/7 global trading venue** offering: - Equities - Commodities - Foreign exchange - Metals - Other traditional assets This implementation demonstrates how decentralized oracle infrastructure can support institutional-grade trading operations around the clock. [Read the full case study](https://www.pyth.network/success-stories/how-hyperliquid-became-the-world-s-24-7-macro-trading-venue-with-pyth?utm_source=organic_social&utm_medium=x_post&utm_campaign=2607_post&utm_term=hyperliquid)

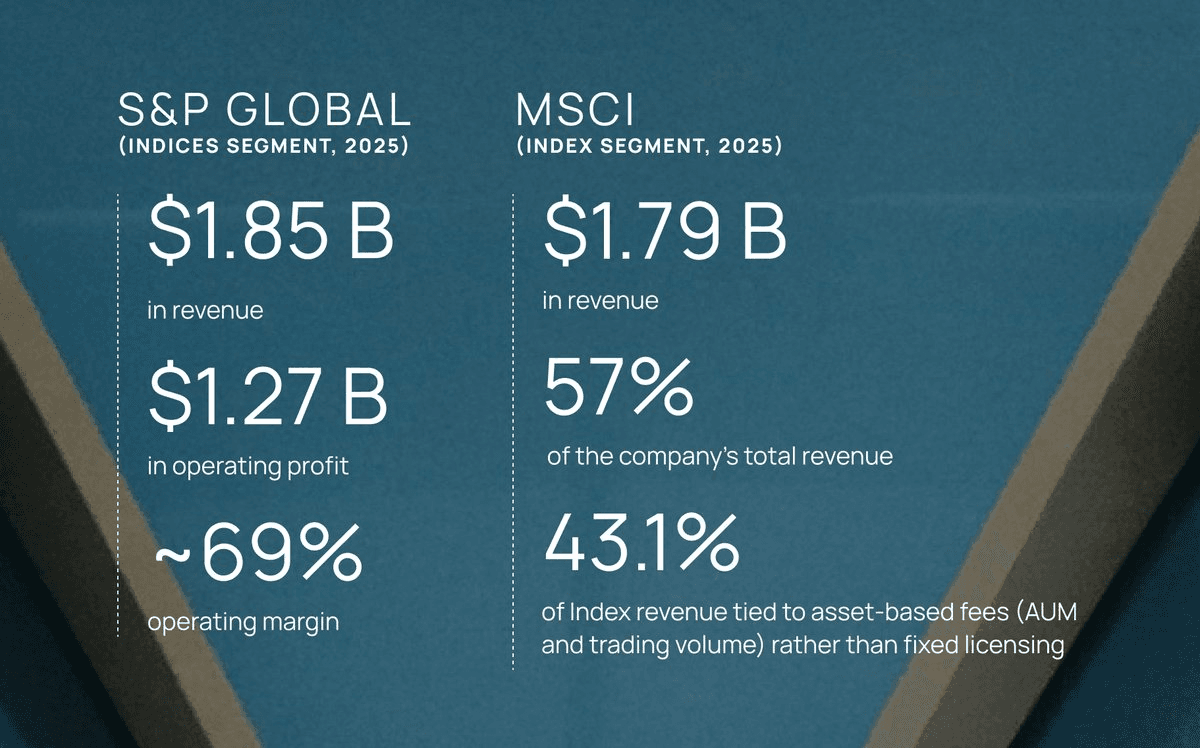

Pyth Indices Launches 24/7 Index Products for Continuous Markets

Pyth is entering the index business by offering continuous, round-the-clock pricing across multiple asset classes. **What's Being Launched:** - 24/7 indices covering equities, foreign exchange, oil, metals, and thematic investment baskets - Continuous pricing model designed for markets that operate without traditional trading hours **Why It Matters:** - The index business represents one of the highest-margin sectors in traditional finance - Pyth is adapting this profitable model for crypto and decentralized markets that never close - Addresses the need for reliable pricing infrastructure in always-on financial environments The move positions Pyth to capture value from index licensing and data provision in the emerging 24/7 financial ecosystem.

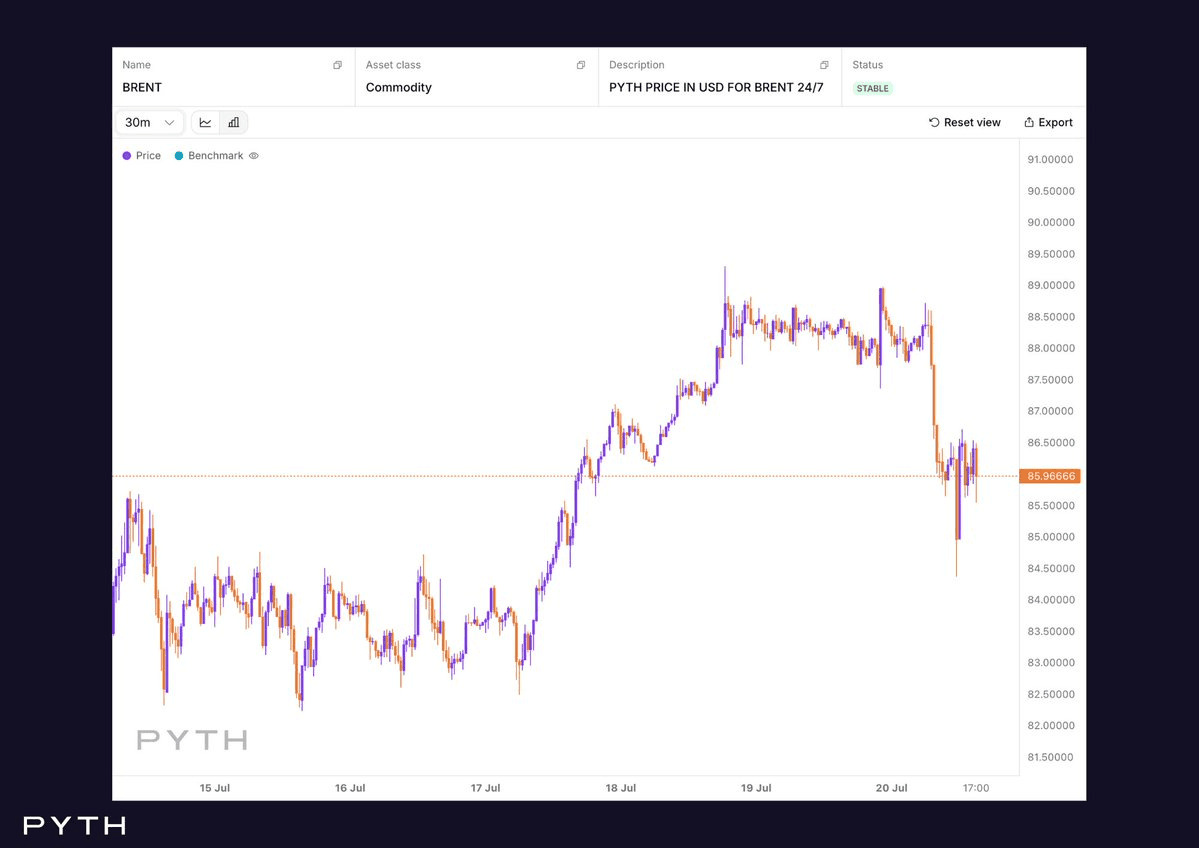

Pyth BRENT Index Tracks Weekend Oil Volatility Amid US-Iran Tensions

**Geopolitical tensions drove energy market volatility over the weekend.** - Brent crude prices spiked as US-Iran escalation raised concerns about potential supply disruptions - The Pyth BRENT Index continuously tracked price movements throughout the weekend period - Market participants monitored the situation closely amid fears of broader impact on oil supply chains The real-time pricing data provided ongoing visibility into market reactions as the geopolitical situation developed.

RWA Markets Dashboard Launch by Zinn Research

A new dashboard tracking Real World Asset (RWA) markets has been launched at rwa-markets.xyz by Zinn Research. The platform provides comprehensive data and analytics for monitoring RWA market activity across the crypto ecosystem. **Key Features:** - Centralized tracking of RWA market performance - Real-time data visualization - Market analytics and insights This tool adds to the growing infrastructure supporting tokenized real-world assets, complementing existing platforms like Pendle Finance's RWA trading markets. [View the dashboard](https://rwa-markets.xyz/)