🔍 Liquity V2 Breaks the Mold: Uncorrelated Borrow Rates in DeFi

🔍 Liquity V2 Breaks the Mold: Uncorrelated Borrow Rates in DeFi

🎯 Breaking the rate herd

Major lending platforms move in lockstep - when Aave spikes, Morpho follows. But Liquity V2 offers a different path.

Key differentiators:

- Average ETH borrow rate: 3.75%

- Rate ceiling: Never exceeded 6%

- Near-zero correlation with major lending markets

- Maintained stability through market crashes and cascades

Why it matters: Traditional DeFi lending rates are highly correlated - when one platform experiences rate volatility, others follow. Liquity V2's independent rate structure means borrowers aren't forced to ride the herd's volatility waves.

The broader context: Recent data shows Liquity V2 consistently offers rates 100+ basis points cheaper than competitors, with wstETH borrowing at just 1.46% - 2% below the next best option. The platform also enables fixed-rate borrowing up to 91% LTV on ETH.

For treasuries and yield optimizers tired of rate unpredictability, this uncorrelated venue presents an alternative to the synchronized movements of pooled lending protocols.

Borrow rates on Aave and Morpho all move together. When one spikes, they all spike. What if there was a venue that was uncorrelated - and cheaper? Liquity V2 ETH rate: 3.75% avg. Never above 6%. Near-zero correlation with every major lending market Your rates don't have to

The best borrow rates in DeFi Liquity V2 consistently offers the lowest borrow rates in DeFi. Not only that, these rates can also be fixed. Rate spikes and volatility make yield optimization and treasury planning cumbersome. Fix your rates: liquity.app/borrow

DeFi borrowing usually breaks at the boring part: you can’t predict your cost. You open at 4%, then the rate spikes because the pool got crowded or parameters changed. That uncertainty kills leverage and treasury planning. Chimera’s point on @LiquityProtocol V2 is that $BOLD

You're paying 5% + to borrow stablecoins. You don't have to. Liquity lowest V2 avg. borrow rates for ETH since launch: 2.82% Next cheapest venue: 4.66% Over 100 bps cheaper. Liquity V2 rates never spiked above 6%. Through every crash and cascade. Control your costs.

Treasuries shouldn’t have to sell ETH to raise runway. With Liquity V2, treasuries can borrow against ETH at a fixed interest rate they choose. The 1yr avg. rates for Liquity V2 is lowest across DeFi by far - a full 2% below the competition. Up to 91% LTV (with ETH) 👇

get paid to borrow with wstETH on Liquity 🔵 It costs 1.46% to borrow against wstETH - 2% cheaper than the next best venue. Why pick Liquity? - You do not overpay - Your rate is not volatile - Your collateral is not lent out @DeFiSaver user? Migrate your loan with one click

Borrow rates are falling. And Liquity V2 has the lowest rates by a wide margin. Why pick Liquity? - You do not overpay - Your rate is not volatile - Your collateral is not lent out @DeFiSaver user? Migrate your loan with one click.

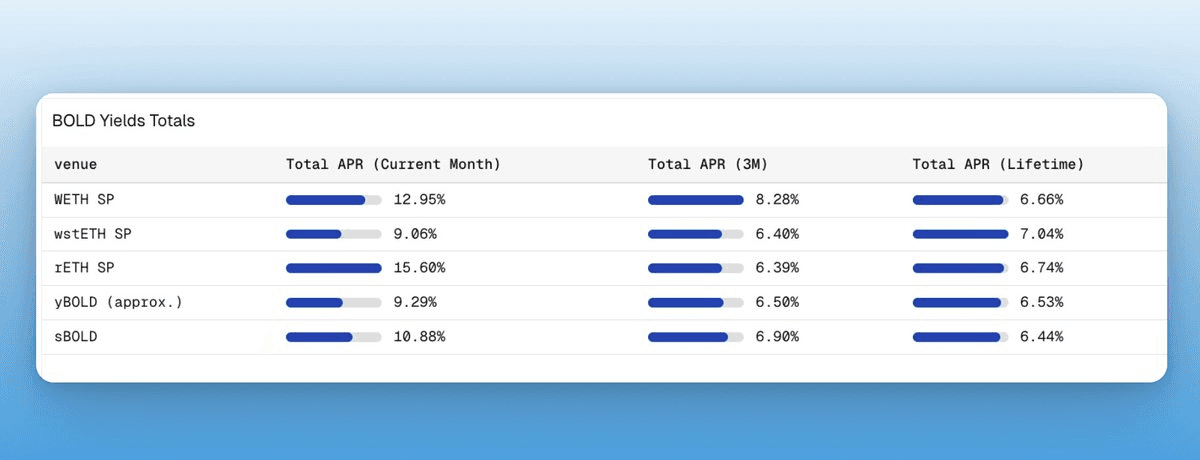

🎯 Liquity V2 Stability Pool Hits 7% Lifetime Yield

Liquity V2's Stability Pool has achieved **7% lifetime yield** since inception, with recent performance reaching higher returns due to increased liquidation activity. **Key Features:** - Zero leverage or duration risk - No counterparty risk or TradFi dependency - Yield paid in BOLD and ETH - 100% of borrower fees passed to users - 75% of fees directed to Stability Pool depositors **How It Works:** Yield comes from crypto-native sources: DeFi borrowing demand and ETH liquidations during market volatility. This creates returns uncorrelated to traditional treasury yields. Unlike T-bill wrappers or lending markets, BOLD offers predictable returns without token emissions, lockups, or vesting requirements. [Learn more about Stability Pool mechanics](https://www.liquity.org/blog/liquity-v2-bold-stability-pool-opportunities)

DeFi Saver Loan Shifter Enables Cross-Platform Loan Migration

**DeFi Saver** has launched its **Loan Shifter** functionality, allowing users to migrate loans between different DeFi platforms. **Key Features:** - Seamless loan transfers across protocols - Rate arbitrage opportunities - One-click liquidation price adjustments - Compatible with smart wallets The tool aims to help users optimize their borrowing costs and manage risk more effectively by providing flexibility to move positions between platforms. [Access Loan Shifter](https://app.defisaver.com/shifter)

🚨 DeFi Yield Risks vs BOLD

A stark comparison highlights common DeFi yield risks versus BOLD's approach. **Typical DeFi Yield Risks:** - Multi-sig fund custody with anonymous teams - Governance tokens as yield (often locked) - Undercollateralized market maker loans - Weekly deployment to new yield venues - Offshore entities with unclear jurisdiction - Cross-chain bridge exposure - Secondary oracle dependencies - Exposure to 6+ additional protocols - CEX carry trade risks **BOLD's Alternative:** - Immutable code (no counterparty risk) - Clean collateral: WETH, wstETH, rETH only - No rehypothecation - funds stay in Stability Pool - Ethereum-only (no bridge risk) - No governance changes possible - Zero TradFi or CEX exposure - Stablecoin yield payments **Remaining Risks:** - Smart contract risk (mitigated by 5 audits) - Oracle risk (Chainlink dependency) The post questions whether complex yield strategies justify their risk profiles.

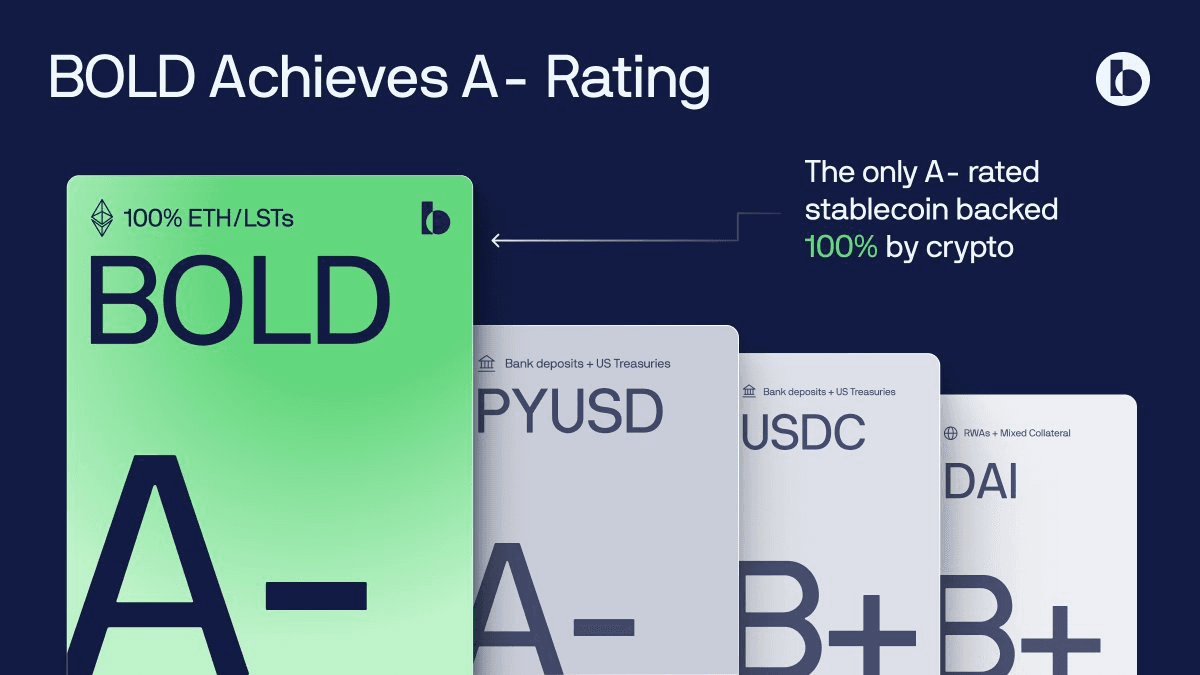

BOLD Stablecoin Achieves A- Rating from Bluechip, Outranking USDC and DAI

**BOLD has secured an A- rating from Bluechip**, making it the only crypto-native stablecoin to reach A-tier status. This rating surpasses both USDC and DAI, which received B+ ratings. **Key achievements:** - Perfect 1.0 scores in three critical areas: Management (immutable), Decentralization (no admin keys), and Governance (no governance) - Higher rating than established stablecoins USDC (B+) and DAI (B+) - Independent validation confirms BOLD's trustless design The rating reflects BOLD's commitment to decentralization and immutability. Unlike traditional stablecoins, BOLD operates without freeze functions, blacklists, or upgrade capabilities, ensuring users maintain full control of their assets. Full rating details available at [Bluechip's official assessment](https://bluechip.org/en/coins/bold).