BitGo Enables Institutional Access to Multi-Venue On-Chain Credit Through Spark

BitGo Enables Institutional Access to Multi-Venue On-Chain Credit Through Spark

🏦 Institutions go multi-venue

Institutional capital held in custody can now access on-chain credit markets through BitGo's integration with Spark.

How it works:

- Capital deploys into Spark Savings vaults via BitGo institutional wallets

- Funds are allocated across multiple credit venues within a structured system

- Allocation follows predefined liquidity, exposure, and parameter rules

Key difference from traditional on-chain lending: Most platforms require choosing a single market or pool. Spark distributes capital across venues automatically, reducing exposure to high-utilisation conditions where liquidity becomes constrained.

This marks a new pathway for institutional capital into on-chain credit markets without requiring direct on-chain operations.

Institutional capital held in custody can now now access on-chain credit markets through structured allocation via Spark. Through BitGo, capital can be deployed into Spark Savings vaults, where it is allocated across multiple credit venues within a single, structured system.

Spark Prime Integrates RedStone for Institutional Crypto Lending

Spark Prime, the institutional crypto lending platform, has integrated with RedStone to support institutional borrowers like Anchorage. **Key Integration Details:** - RedStone integration is a vital component of Spark Prime's infrastructure - Enables institutional-grade crypto borrowing services - Supports Anchorage and other institutional clients **About Spark Prime:** Launched in February 2026, Spark Prime is a CeDeFi margin lending platform powered by Arkis's margin technology. The platform offers: - **Enhanced security**: Over-collateralized positions for more resilient delta-neutral lending - **Capital efficiency**: Improved efficiency compared to traditional DeFi lending markets - **Transparency**: Real-time position visibility through protocol-level data The platform enables institutional borrowers to deploy collateral seamlessly across both DeFi and CeFi venues, addressing the opacity issues common in traditional funds.

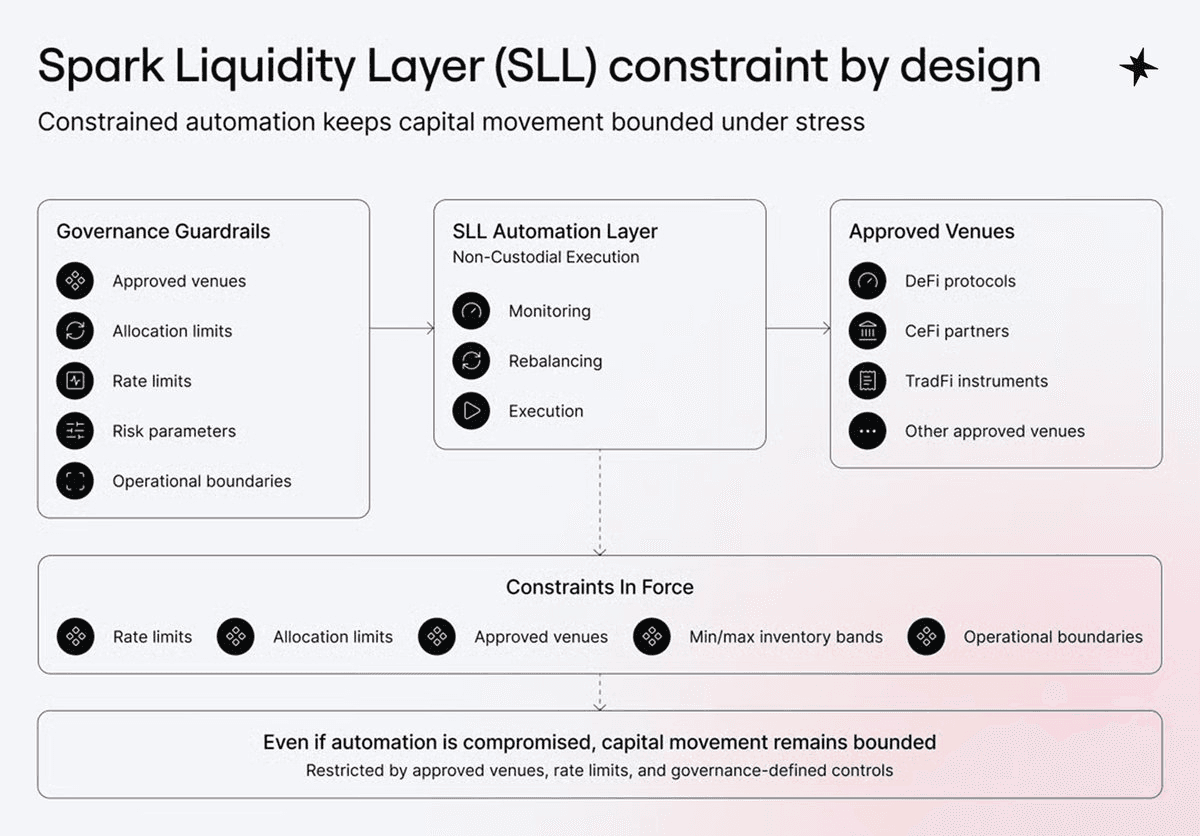

Spark's Security Framework: Bounded Automation for Institutional Liquidity

Spark Liquidity Layer introduces a security model where automation operates within strict governance-defined boundaries. The system uses three constraint layers: - **Approved venues** limit where capital can move - **Allocation and rate limits** control how much moves and at what speed - **Min/max inventory bands** cap holdings per venue The key security property: even if automation is compromised, capital movement remains bounded by pre-execution constraints. For institutional infrastructure, trust lies in the constraint system itself, not the automation layer. This approach solves liquidity orchestration's core challenge—enabling fast capital movement across venues without creating unbounded exposure risk. [Read full security framework](http://paragraph.com/@spark-11/spark-security-framework)

Spark Savings Integrates Natively Into Rabby Wallet for Direct Yield Earning

Spark Savings has launched native integration within Rabby wallet, allowing users to earn yields on USDS, USDC, USDT, and ETH without leaving their wallet interface. **Key features:** - Direct earning on idle assets within Rabby - No bridges or additional steps required - Instant redemption capability - Protected by Spark Savings Risk Framework with risk absorption layers The integration represents a shift in wallet functionality—from simple asset storage to active capital management. Users can now put idle funds to work while maintaining the security and convenience of their trusted wallet environment. The service supports multiple stablecoins and ETH, with deposits processed in approximately 60 seconds through a straightforward interface.

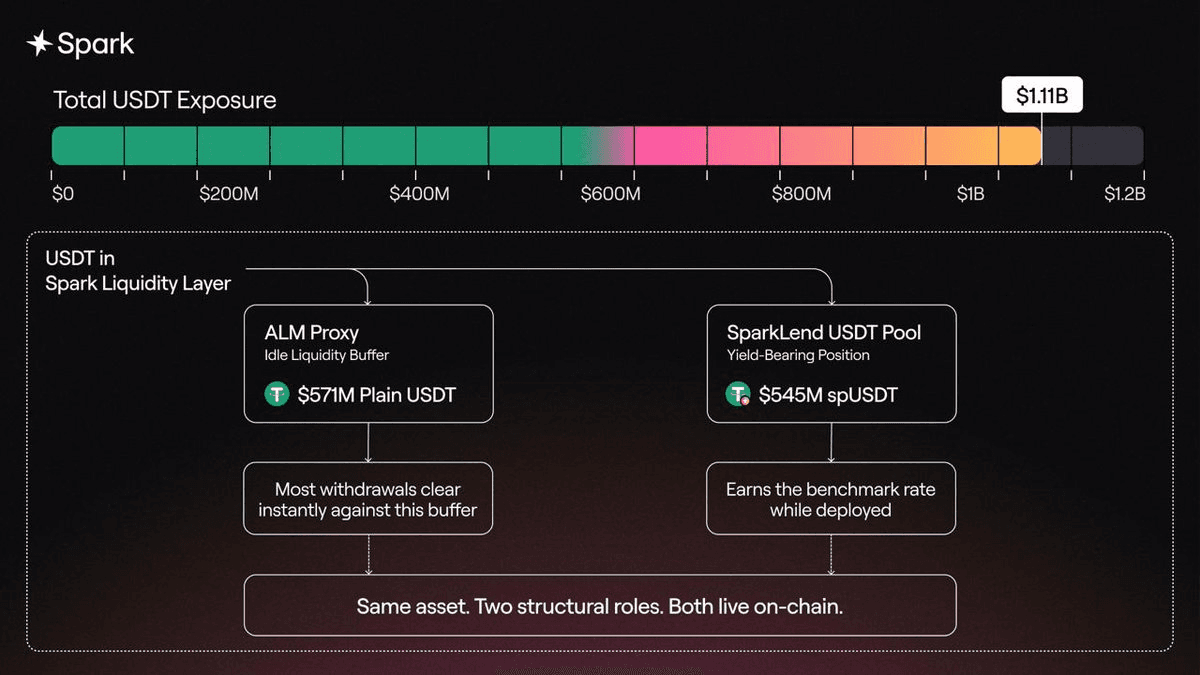

Spark's $1.11B USDT Liquidity Layer: How Two-Role Capital Split Solves the Deployment vs. Liquidity Dilemma

**The Core Challenge** Credit markets face a fundamental tradeoff: hold too much capital in reserve and returns drop; deploy too much and liquidity dries up. **Spark's Two-Role Solution** Spark's Liquidity Layer manages $1.11B USDT through a strategic split: - **$571M in plain USDT** sits in the ALM proxy as an idle liquidity buffer, enabling instant withdrawals for most users - **$545M deployed as spUSDT** into SparkLend's USDT pool, earning the benchmark rate **Why It Matters** This dual-role structure allows Spark Savings USDT to simultaneously offer: - Real liquidity depth for withdrawals - Competitive returns through active deployment - Larger exits handled through a request flow when needed The approach demonstrates how the same asset can serve different functions—immediate availability and yield generation—without forcing users to choose between liquidity and returns. [Deposit USDT](https://app.spark.fi/savings/mainnet/spusdt)

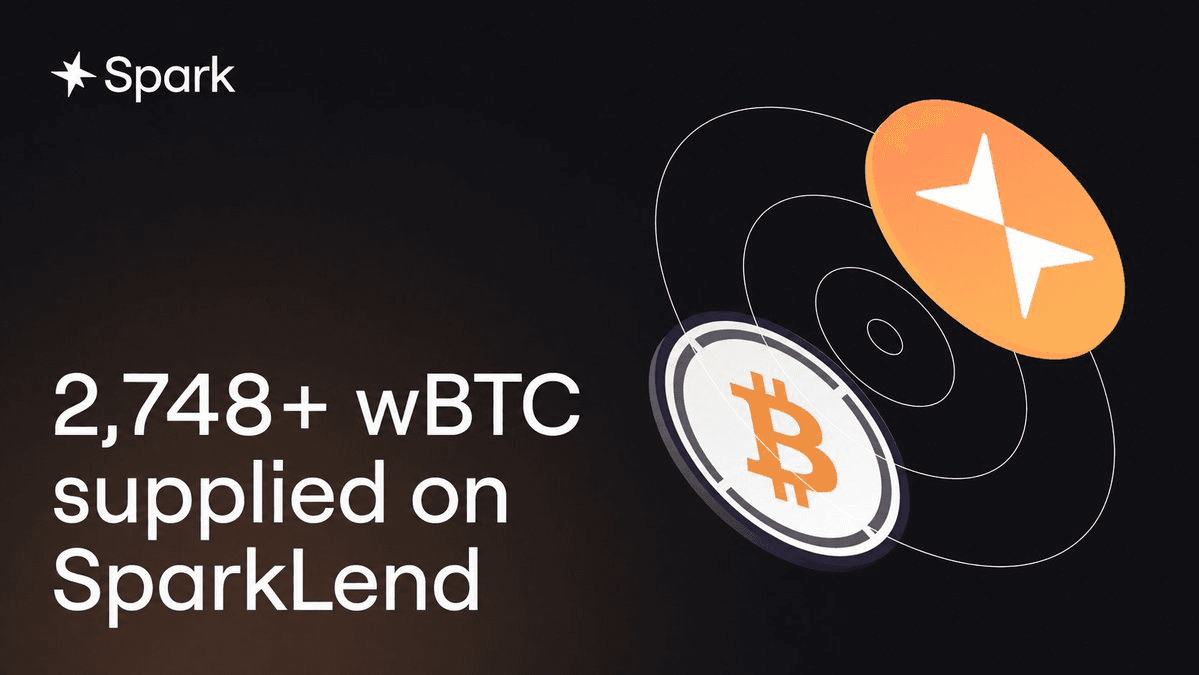

SparkLend Attracts 2,748 wBTC in Three Days Following March Launch

SparkLend has accumulated over 2,748 wBTC as collateral since launching in March, with the majority arriving within a three-day period as borrowers refinanced existing positions. **Key developments:** - Initial 3,000 wBTC deposit cap reached quickly, prompting an increase to 30,000 wBTC - New capacity opens gradually at 500 wBTC every 12 hours through cap automator mechanism - Rapid adoption indicates strong demand for BTC-backed borrowing venues The swift capital migration suggests the market was waiting for infrastructure rather than lacking demand. Borrowers can access the platform at [app.spark.fi/borrow](https://app.spark.fi/borrow).